Part 3 in FinCred’s Credit Risk Management series

Parts 1 and 2 of our series on Credit Risk Management looked at identifying and analysing risks to your business, and how to spot the warning signs a customer or prospect might be struggling.

But how risky is your new prospect? What steps can you put in place to maximise your trading potential? How can credit risk management boost the growth of your business?

In Part 3, FinCred explains the process of evaluating and treating credit risk.

Evaluating the Credit Risk

Evaluation is a vital step in the credit risk management process. This means weighing up the knock on effects should a customer fail to pay an invoice. What is the financial impact on your company? How severe is the risk? Can your business absorb the cost?

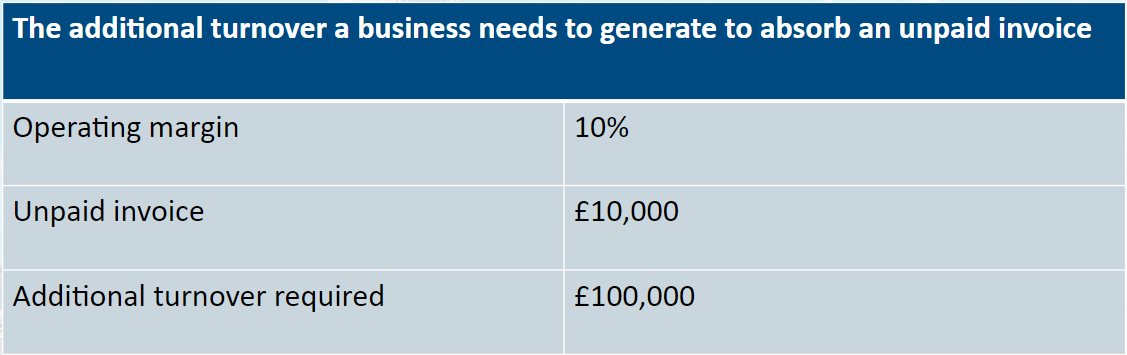

Let’s look at an example. Company A is a manufacturing business that trades on credit terms with Company B. Company A operates with a 10% profit margin. In the event that Company B fails to pay an invoice of £10,000, Company A would need an additional £100,000 turnover to absorb the unpaid invoice.

If the unpaid invoice was £20,000, an additional £200,000 turnover would be needed, and so on.

Treating the Credit Risk

Credit risk treatment generally involves a cost analysis and a combination of procedures based on the financial impact if the credit risk is realised.

Avoid

Once you have identified, analysed and evaluated the severity of the credit risk, the first strategy is to avoid. This might be trading with companies on a cash only basis. This avoids a scenario where another business may owe you for services or goods already delivered.

Selling on a cash basis offers you the benefit of avoiding risk altogether, but may also put you at a significant competitive disadvantage. FinCred details the benefits of trading on credit terms in our blog How Trade Credit Insurance Can Boost Your Business Profits and Growth.

Mitigate

Once you decide to trade on credit terms, it is crucial to mitigate the associated risks with a robust credit risk management strategy. This involves thorough analysis and due diligence of both prospective and existing customers.

Institutions such as a trade credit insurance company can offer a wealth of information that can strengthen your risk management process. This can be seen as an extension of your own due diligence and credit risk analysis, enhancing your evaluation and assessment.

You may still be at risk of unexpected insolvencies or sudden non-payments, even once you understand your business’ credit risks and have a robust credit control policy in place. So what are your options?

Transfer

There are a number of risk transfer options available to your business.

- Self Insurance

Many companies set aside a cash reserve to service bad debts, enabling them to offset a deficit should any invoices go unpaid. Businesses should ensure that they have credit management resources, systems and data which provide real time analysis of credit risks if they are self-insuring.

It’s important to understand this method may impact your sales and working capital. If the bad debt is significant or large, it is possible that the reserves will not be large enough to cover a catastrophic loss.

- Invoice Finance

A second option is to finance your invoices. Invoice finance companies purchase invoices at a reduced amount including a fee, giving you access to funds before your customers pay you.

In some cases, the company will also take on the risk of non-payment of the invoices purchased (non-recourse finance). In others, you will need to mitigate this risk and be able to reimburse funding if the customer does not pay (recourse finance).

- Letter of Credit

A letter of credit is a promise by a bank that the payment will be made, provided goods are shipped on time with the correct paperwork. In short, it provides certainty that you will be paid for goods you export. In this scenario, the risk of non-payment is transferred to the bank.

Cash can be required by the buyer as security in some developing markets. Coverage is for a single transaction for a single customer. As a result, it can be time consuming and expensive across a whole export portfolio.

- Trade Credit Insurance

Trade credit insurance reimburses your business when customers are unable to pay due to insolvency, default or political conditions. It provides financial protection against unpaid invoices, along with a number of other benefits including:

- Cash Flow Protection – Indemnifies your losses and protects you against fluctuations in cash flow.

- Boosts Business Growth – Provides capacity to increase order volumes and sales.

- International Expansion Opportunities – Protects export risks, reducing uncertainty for companies.

- Frees Up Capital – Reduces the need for large bad debt reserves, allowing you to reinvest the funds in your business.

- Facilitates Funding – Banks offer more favourable lending terms to businesses that insure their accounts receivable.

- Credit Risk Management – Analyse and evaluate your customers via the insurers in-depth knowledge of sectors, companies, markets and trends.

FinCred details how bad debt protection can improve your credit risk management in our full breakdown of trade credit insurance.

Accept

Following a thorough analysis and evaluation, a combination of mitigation and transference should provide a comfortable level of acceptance, knowing that services such as trade credit insurance will indemnify your losses should a customer become insolvent.

Monitor and Review

The final stage of a robust credit risk management process is to monitor and review. This involves regular assessment and reassessment of stages 1 to 5 of the process: identify, analyse, evaluate and treat.

What Happens Next?

Contact us today if you want a no obligation chat about how trade credit insurance can improve your credit risk management strategy.